>Mitchell and Edon v Ross, [1961] 40 TC 11 (CA) 61

Citation:>Mitchell and Edon v Ross, [1961] 40 TC 11 (CA) 61

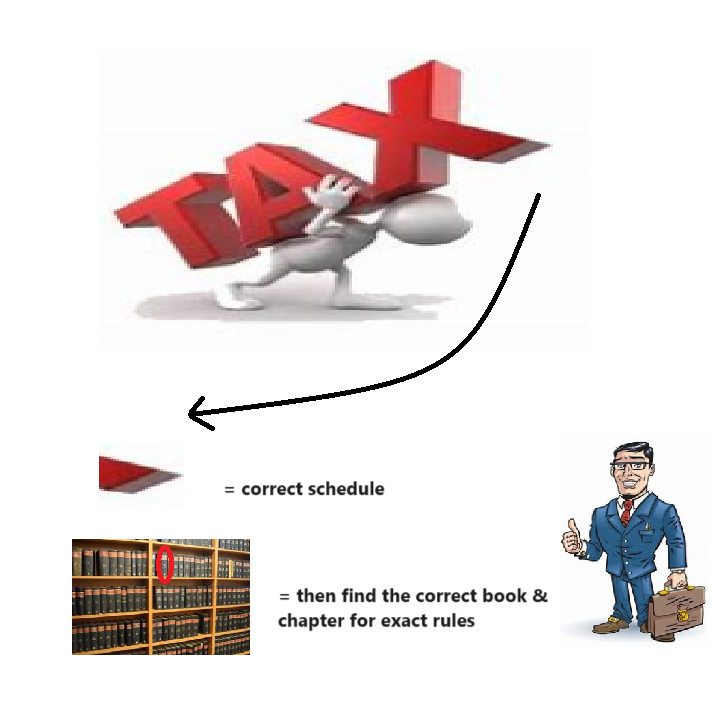

Rule of thumb: What is the basic way that tax-law works? All people & organisations must fundamentally find the correct general ‘schedule’ they are in, and then do their best to follow the particular rules within that schedule.

Judgment:

“Before you can assess a profit to tax you must be sure that you have properly identified its source or other description according to the correct Schedule: but, once you have done that, it is obligatory that it should be charged, if at all, under that Schedule and strictly in accordance with the rules that are there laid down for assessments under it. It is a necessary consequence of this conception that the sources of profit in the different Schedules are mutually exclusive’, Lord Radcliffe

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.