Wimpy International v Warland, 1988, 61 TC 51

Citation:Wimpy International v Warland, 1988, 61 TC 51

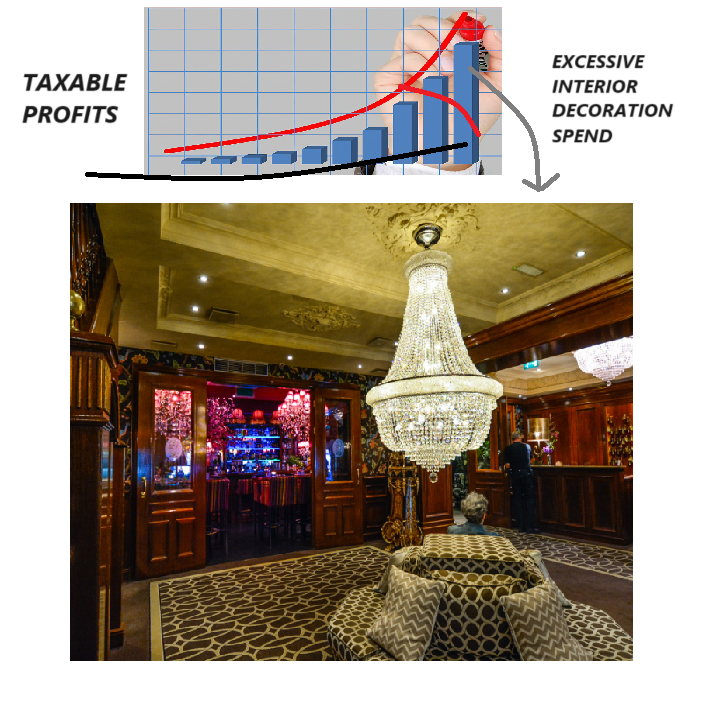

Rule of thumb:Is there a limit to how much investment in refurbishments is tax-deductible? Yes, once self-investment in refurbishing & assets goes above it a certain level, it is no longer tax deductive.

Judgment:

The facts of this case were that Wimpy and Associated Restaurants both did a whole lot of work in refurbishing their restaurants – this included new doors, partition floors, a new ceiling, decorative items, flashy lights etc. They both had cases heard at the same time as guidance was sought on the law in this area. It was held that not all of these were considered to be investment in ‘plant’ and others were considered to be investments in property, which were under 2 different tax schedules, ‘It is proper to consider the function of the item in dispute. But the question is what does it function as? If it functions as part of the premises it is not plant.’ Lloyd LJ

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.