Kennedy v Norwich Union Fire Insurance Society Ltd 1993 S.C.578, EWCA

Citation:Kennedy v Norwich Union Fire Insurance Society Ltd 1993 S.C.578, EWCA

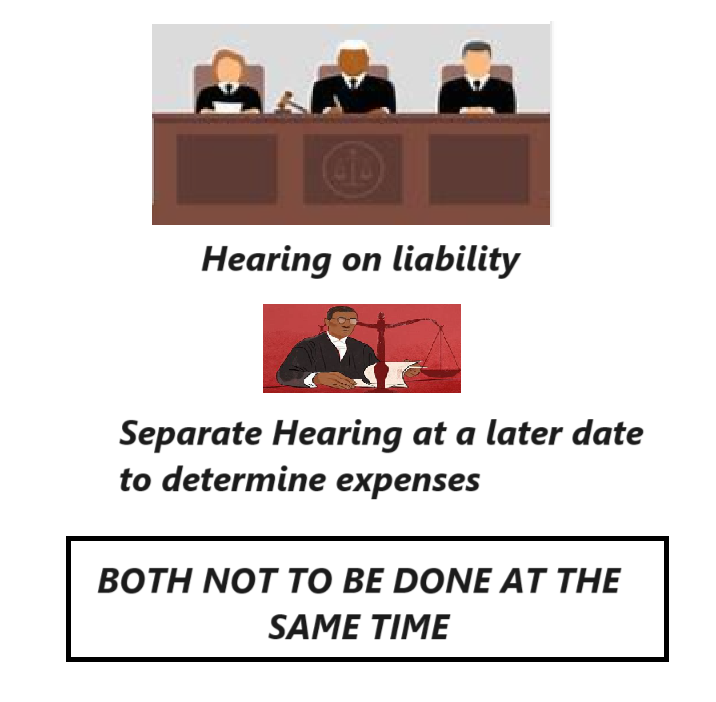

Rule of thumb: Can the issue of expenses owed by a losing party be dealt with in the same Judgment as the decision on liability? No, there has to be a separate Hearing on expenses.

Judgment:

There is a ‘loser pays’ expenses system in place, and the trial Judge can affirm whether a party in the litigation is entitled to expenses or not, but people are entitled to a full hearing in order to ascertain exactly what the expenses should be, ‘in respect of the defenders’ preliminary plea... the defenders had been very substantially successful in the debate and were entitled to their expenses... In the course of the discussion I voiced concern that the defenders, whose expenses are covered by the Master Policy insurers, might seek to enforce any awards I might make against the pursuer, a privately funded individual, before the conclusion of the action. This might be done in an effort to force the pursuer to abandon the action. I asked the defenders' counsel for an undertaking that any award would not be so enforced. She said that she had no authority to give such an undertaking. I could have avoided the potential issue by reserving the question of expenses but I thought it better that I deal with the issue of expenses now as I hope to pass the management of this case to one of the other commercial sheriffs as soon as possible.... Accordingly I said that I would make a finding in favour of the defenders but refrain from including in the interlocutor the usual formula allowing the defenders to make up an account, lodge it in process and upon this being done remit the account to the auditor of court to tax and to report. By so doing would achieve the same result as the undertaking which I sought. At the conclusion of the action, or at some other juncture then thought appropriate, whichever sheriff is then dealing with the case should be able to allow the defenders to lodge an account and then remit it to the auditor for taxation....... In the context of a commercial action under Chapter 10 (sic) it seems to me that what I did is an entirely appropriate exercise of judicial discretion".

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.