Revenue and Customs v Coal Staff Superannuation Scheme Trustees Ltd [2022] UKSC 10 (27 April 2022)

Citation:Revenue and Customs v Coal Staff Superannuation Scheme Trustees Ltd [2022] UKSC 10 (27 April 2022).

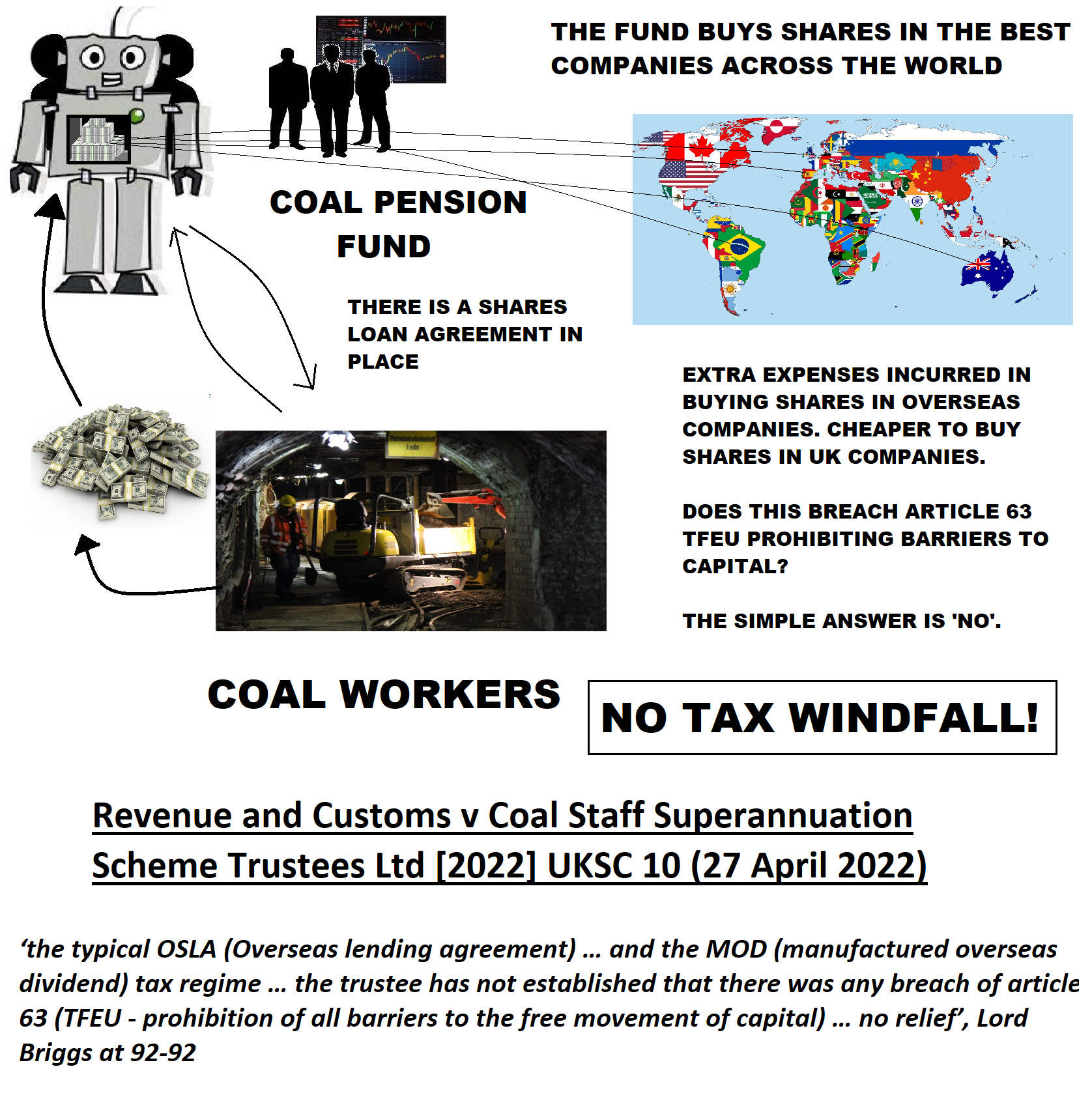

Subjects invoked: '55. Investments','80. Income Taxes',

Rule of thumb:Are pension/investment funds who buy shares overseas entitled to write off the additional costs of doing this as tax deductible expense? To cut a long story short – no. There are long and complex accounting reasons for why these fees are justified upon foreign companies but not UK based ones.

Background facts:

This case invoked the subjects of ‘professional services – investments’, and ‘income tax’. The issue in this case was whether the additional fees people’s investors in the UK had to pay on dividends from foreign companies breached Article 63 of the Treaty for the Functioning of the European Union - ‘The prohibition of all barriers to the free movement of capital’.

The material facts of this case were that there was a pension-fund which had many clients, who all worked in the coal mining industry, giving them money to invest for them. The trustees running this pension-fund essentially took their clients’ money and bought shares in the best companies across the world for them. One of the technical strategies used by the investors under this investment was ‘shares loans’. Rather than the pension-fund be the owner of the shares on the register of the companies they bought shares in, their clients would be the named shareholders on the shares register for the company. However, their client would then loan these shares to the investors in the pension fund who were tax exempt, and they would handle all work & business in relation to them. The contract between investors and trustees to bring this into force with UK companies was called a ‘shares lending agreement’ (SLA), and the contract between investors and trustees to bring this into force with foreign companies was called an ‘overseas shares lending agreement’ (OSLA). When this was done between investors/trustors and trustees/investees for UK companies it was called a ‘manufactured dividend’ (MD), and when this was done with foreign companies it was called an ‘manufactured overseas dividend’ (MOD).

A problem came because basically this arrangement led to more fees being incurred on dividends from overseas companies (MOD’s) as compared to dividends from UK companies (MD’s) i.e. investors were more likely to buy shares in UK companies rather than from foreign companies because there were less fees involved. The investment fund wanted to deduct these extra fees incurred from MOD’s to be deductible from their clients’ income. They were seeking a big tax rebate for this as well. HMRC maintained that their system for dealing with this was correct with the additional fees correctly imposed and no refund owed.

Judgment:

The Court upheld the arguments of HMRC. The additional fees to be paid on dividends received from foreign companies (MOD’s) were not deemed to be deductible and were there for justifiable reasons. There are no tax rebates being paid on the extra fees incurred from foreign company dividends. The mechanics of how this whole arrangement worked was very complex; the rationale for the Court’s decision that this did not breach Article 63 was also very complex (both were also virtually impossible to decipher from the Judgment without accounting knowledge). Frankly this case was unsuccessful and the bottom-line is that this matter is a non-runner for people looking to claim tax rebates from HMRC. It was essentially all much ado about what turned out to be nothing in the end.

Ratio-decidendi:

’92. To summarise the position: (i) the typical ‘Overseas Shares Lending Agreement’ (OSLA) visited upon lenders the reduction of their ‘Manufactured Overseas Dividend) MOD below a payment of the gross equivalent of the dividend by reference to, and only because of, the foreign withholding tax, since that is what it was designed to, and did, do; (ii) without the MOD tax regime, a lender would have suffered the effect of the foreign withholding tax, in terms of reduced MOD payments, without any corresponding double taxation relief in the form of a tax credit of the type available if the relevant overseas shares had been retained by the lender (ie a credit useable only to set off against an income tax liability); (iii) the MOD tax regime remedied that precisely by providing a tax credit “in respect of foreign withholding tax”, and this was a matter of substance (indeed, a critical substantive effect intended to be produced by the MOD tax regime), not fiction; (iv) true it is that the MOD tax regime also imposed a tax on the borrower (the MOD WHT) which was calculated on a “deduction at source” basis involving the pretence that the pre-tax entitlement of the lender was to the full grossed up dividend equivalent, but that really was a fiction, because the lender had no contractual entitlement to the gross sum; (v) in fact, therefore, the MOD WHT neither impoverished the lender (who did not pay it, nor suffered any diminution of its MOD entitlement by reason of it) nor enriched the Revenue, because the borrower always set it off against a wide range of tax credits. There is, therefore, no basis for application of the extended San Giorgio principle in relation to the full amount of the tax credits in issue…. the claim as framed by the Trustee must fail … Lord Briggs at 92-93

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.