Mcknight (Her Majesty's Inspector of Taxes) v Sheppard [1999] UKHL 6 (17 June 1999)

Citation:Mcknight (Her Majesty's Inspector of Taxes) v Sheppard [1999] UKHL 6 (17 June 1999)

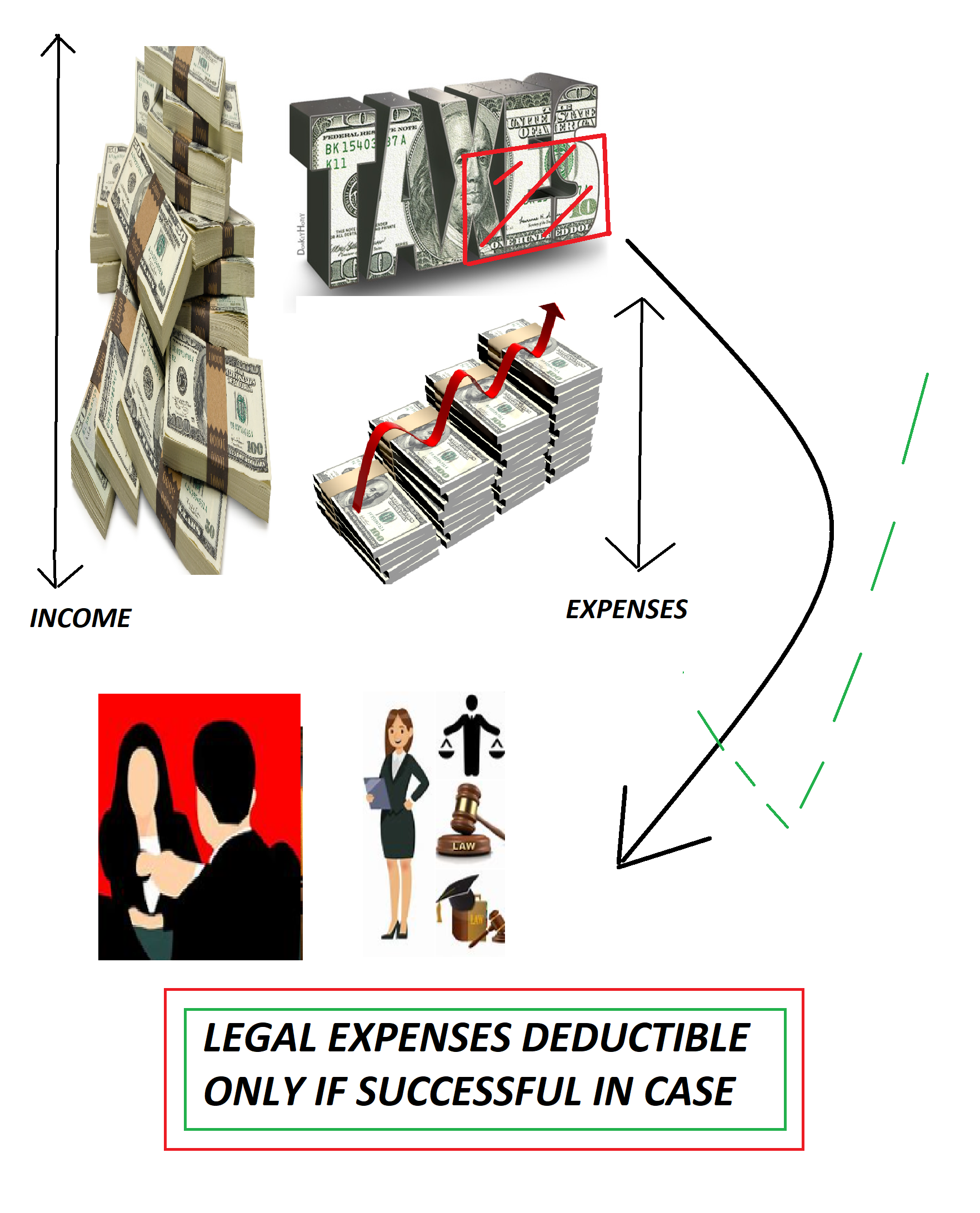

Rule of thumb:Are legal fees a deductible expense for tax? Only if they are reasonably incurred. A successful case or a controversial one with contrasting legal advice.

Background facts:

A number of complaints were raised against the stock broker and £200,000 was incurred by the stock broker in legal fees defending professional misconduct proceedings.

Judgment:

The Court held that these expenses were deductible in computing the organisation’s profits as they were reasonable incurred.

Ratio-decidendi:

’...Mallalieu v Drummond, at pages 365 - 366 is illuminating. The relevant passage is as follows “... it is only expenses incurred ... wholly ... and exclusively ... in association with the trade... which are tax deductible...’ If Lord Brightman’s consultant had said that he had given no thought at all to the pleasures of sitting on the terrace with his friend and a bottle of Côtes de Provence, his evidence might well not have been credited. But that would not be inconsistent with a finding that the only object of the journey was to attend upon his patient and that personal pleasures, however welcome, were only the effects of a journey made for an exclusively professional purpose. This is the distinction which the Special Commissioner was making and in my opinion there is no inconsistency between his conclusion of law and his findings of fact.... the reason in my opinion …relates to the particular character of a fine or penalty. Its purpose is to punish the taxpayer and a court may easily conclude that the legislative policy would be diluted if the taxpayer were allowed to share the burden with the rest of the community by a deduction for the purposes of tax…I think that the Special Commissioner and the Judge were quite right in not allowing the fines to be deducted. It does not follow, however, that the costs were not deductible. Once it is appreciated that, in a case like this, non-deductibility depends upon the nature of the expenditure and the specific policy of the rule under which it became payable, it can be seen that the relevant considerations may be quite different.’ Lord Hoffman

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.