Caparo Industries pIc v Dickman [1990] 2 AC 605

Citation:Caparo Industries pIc v Dickman [1990] 2 AC 605

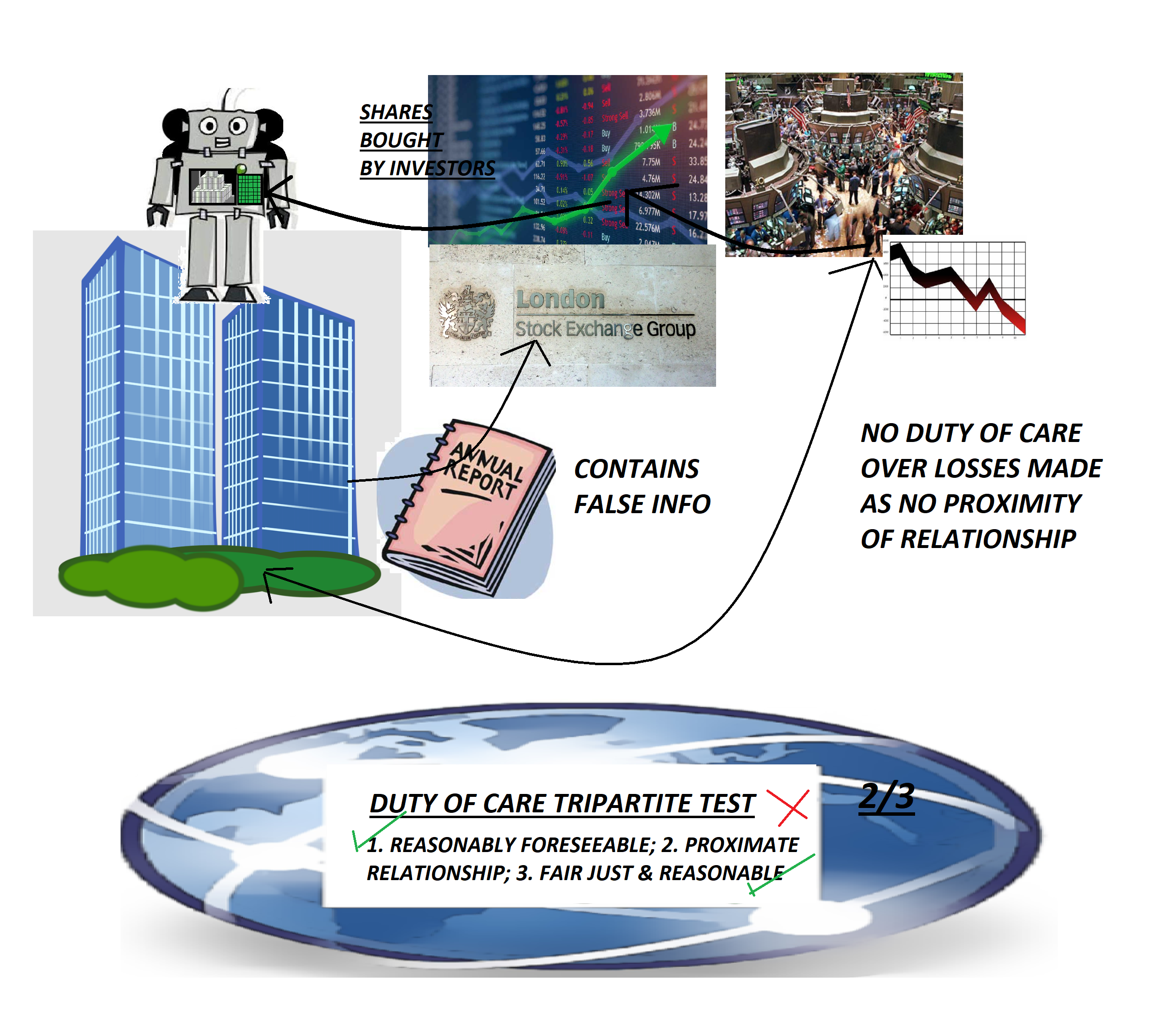

Rule of thumb:What is the basic test of proving liability against another party for pure economic loss? This case established a 3 part test for establishing a breach of the duty of skill and care – (1) reasonably foreseeable, (2) proximate relationship, and (3) fair just and reasonable. Parts 1 and 3 of the test are not so significant – (1) there was no scientific evidence at the time to suggest it was impossible, (2) that there is a significant relationship between the 2 parties, to make a connection, with an injury caused by one to the other sufficient to create this, and (3) is that a primary law source has to be relied on to win a case.

Background facts:

The facts of this case were that Caparo Industries Plc were an engineering company who were doing fairly well and had money in their capital account to potentially acquire other businesses. Fidelity Plc were also engineers and they had issued profit warnings meaning that their share price fell. Caparo bought shares in Fidelity Plc. Fidelity Plc instructed Mr Dickman to provide accounts for them. On the basis of Mr Dickman’s accounts Caparo bought more shares in Fidelity and began the process of a takeover in accordance with the Takeover Code for Public Limited Companies. Upon doing this Caparo discovered that Mr Dickman’s accounts were very misleading and that Fidelity were in far bigger trouble than they realised.

Judgment:

The Court held that although these accounts were quite possibly negligently produced, there was no proximate relationship between Mr Dickman and Caparo meaning that Caparo were not entitled to sue Mr Dickman. Mr Dickman only owed a duty to Fidelity Plc and not an unlimited range of investors.

Ratio-decidendi:

‘I believe it is this last distinction which is of critical importance and which demonstrates the unsoundness of the conclusion reached by the majority of the Court of Appeal. It is never sufficient to ask simply whether A owes B a duty of care. It is always necessary to determine the scope of the duty by reference to the kind of damage from which A must take care to save B harmless. “The question is always whether the defendant was under a duty to avoid or prevent that damage, but the actual nature of the damage suffered is relevant to the existence and extent of any duty to avoid or prevent it:” see Sutherland Shire Council v. Heyman, 60 A.L.R. 1, 48, per Brennan J. Assuming for the purpose of the argument that the relationship between the auditor of a company and individual shareholders is of sufficient proximity to give rise to a duty of care, I do not understand how the scope of that duty can possibly extend beyond the protection of any individual shareholder from losses in the value of the shares which he holds. As a purchaser of additional shares in reliance on the auditor's report, he stands in no different position from any other investing member of the public to whom the auditor owes no duty’, Lord Bridge.

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.