Mallalieu v Drummond 57 TC 330, 1983

Citation:Mallalieu v Drummond 57 TC 330, 1983

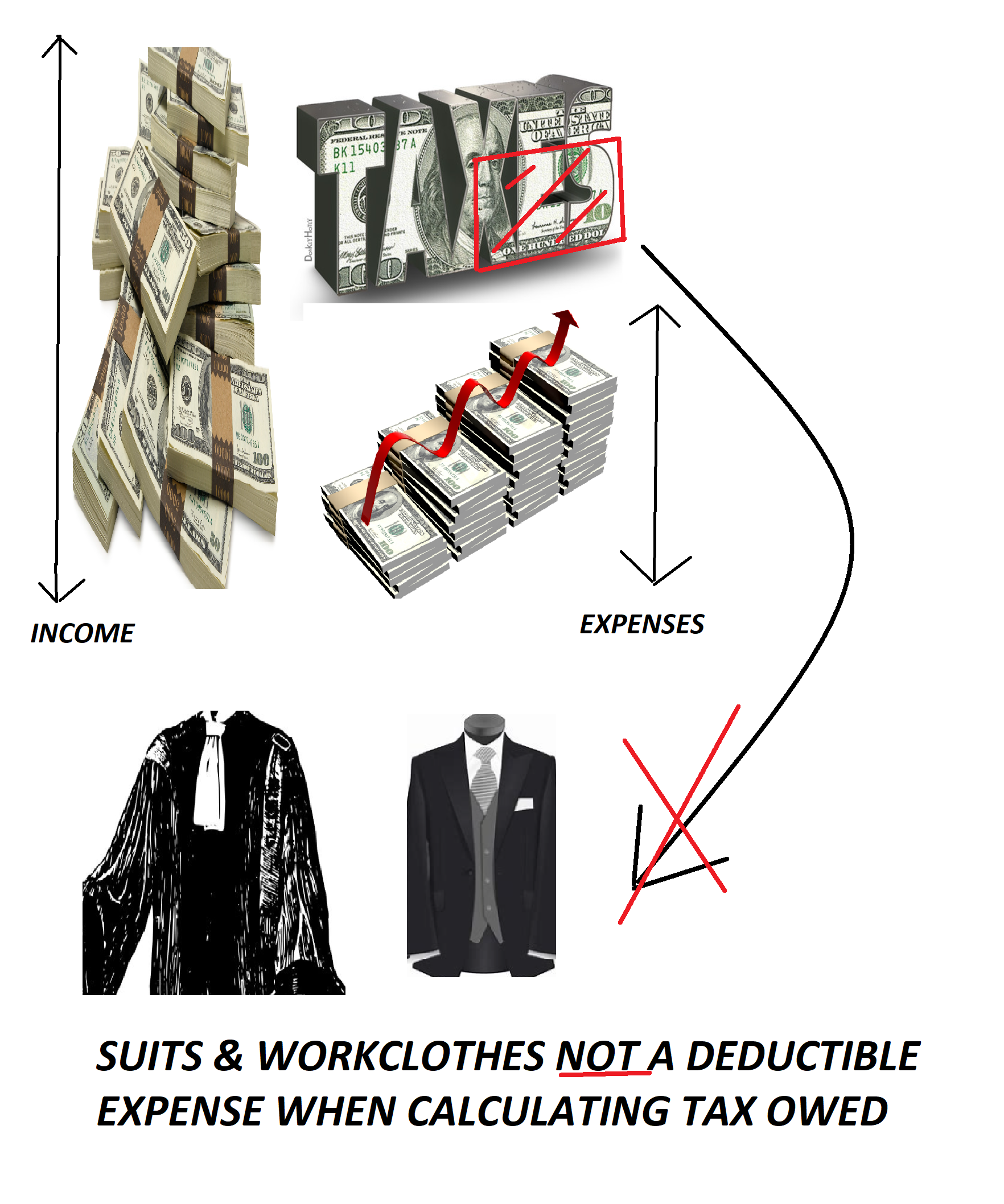

Rule of thumb:Are work clothes, suits etc a deductible tax expense? No, they fail the dual purpose test. They are deemed to serve a dual purpose so do not meet the test of being a deductible tax expense.

Background facts:

The basic facts were a barrister tried to deduct the cost of buying their gown from the amount of money they had to pay tax on.

Judgment:

This case established the ‘wholly and exclusively’ test for whether expenses are deductible or not. A barrister’s gown was not deemed to be a deductible expense because this also served the purpose of decency. The duality of purpose test is that any expense which can serve more than one purpose is not deductible as a taxable expense.

Ratio-decidendi:

‘Of course, the taxpayer thought only of the requirements of her profession when she first bought (as a capital expense) her wardrobe of subdued clothing and, no doubt, as and when she replaced items or sent them to the launderers or the cleaners she would, if asked, have repeated that she was maintaining her wardrobe because of those requirements. It is the natural way that anyone incurring such expenditure would think and speak. But she needed clothes to travel to work and clothes to wear at work, and I think it is inescapable that one object, though not a conscious motive, was the provision of the clothing that she needed as a human being. I reject the notion that the object of a taxpayer is inevitably limited to the particular conscious motive in mind at the moment of expenditure. Of course, the motive of which the taxpayer is conscious is of a vital significance, but it is not inevitably the only object which the Commissioners are entitled to find to exist. In my opinion the Commissioners were not only entitled to reach the conclusion that the taxpayer’s object was both to serve the purposes of her profession and also to serve her personal purposes, but I myself would have found it impossible to reach any other conclusion... ‘such cases are a matter of fact and degree’. Lord Brightman

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.