Bullock v Unit Construction, 1959, [1959] UKHL TC – 38 – 712

Citation:Bullock v Unit Construction, 1959, [1959] UKHL TC – 38 – 712

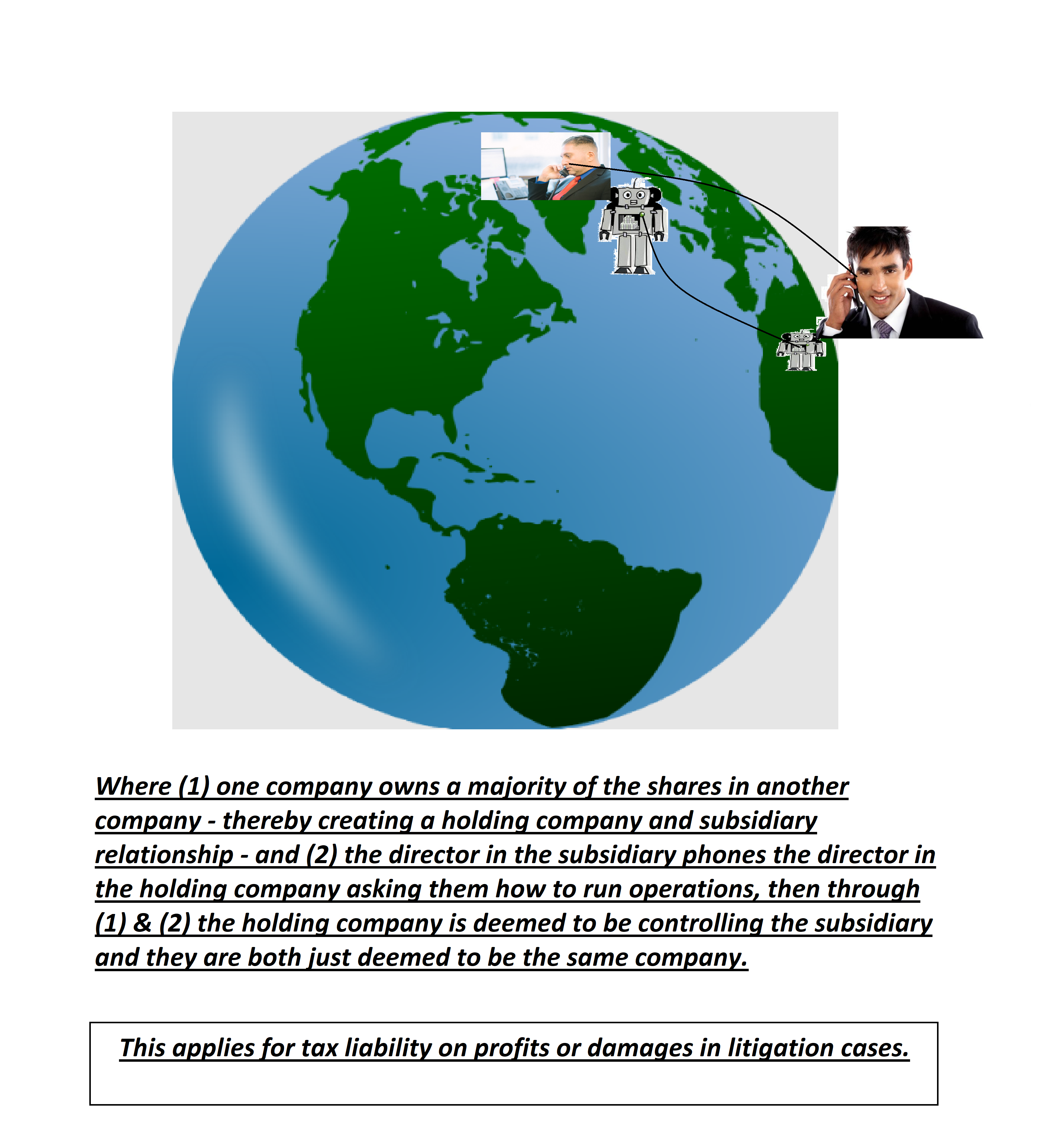

Rule of thumb:If a company is registered abroad, does it mean this is where the company is run from? No, the company is run from the place where management decisions are taken.

Judgment:

Where there is a subsidiary of a country abroad, and day to day decisions regarding its operations are taken there, but, the major decisions regarding its general direction & operations are taken in the UK, then these subsidiaries wll be treated as UK companies due to pay tax in the UK. Where the managers are & where the decisions are being made will be deemed to be where a country is based.

Ratio-decidendi:

‘The Commissioners are not, I think, concerned with whether the powers of directors of a company are exercised in accordance with the constitution of the company. If the actings of a person or corporation are such as to attract liability to tax or give some entitlement to relief from tax, so long at least as these actings are not a facade to cover a reality which has a different result, the Commissioners have, I think, no concern with the legality, or otherwise, of these actings. It is the facts of the case that have to be considered with the legal results that follow. For that reason I could not agree with the ratio of the decision of the Court of Appeal. But when the facts of this case are considered I feel considerable doubt whether they establish that the “ African subsidiaries ” were at the material times resident in the United Kingdom. What they show is that another company, Alfred Booth & Co., Ltd., resident in London, through its board, exercised the real management and control of the African subsidiaries. There is no suggestion that it was authorised so to do by the boards of the African subsidiaries. It is true that Alfred Booth & Co., Ltd. was the parent company and controlling shareholder of the subsidiary companies, but that does not avoid the fact that it was a different person from the African subsidiaries. I should have thought, therefore, that there might be a question whether the African subsidiaries could be said to be in any sense resident in the United Kingdom in respect that no actings of theirs could be said to show that the central management and control actually abided there’. Lord Keith

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.