Revenue and Customs v NHS Lothian Health Board (Scotland) [2022] UKSC 28 (19 October 2022)

Citation:Revenue and Customs v NHS Lothian Health Board (Scotland) [2022] UKSC 28 (19 October 2022).

Subjects invoked: 8. 'Evidence'.14. 'Remedies'.81. 'Transactional Taxes'.

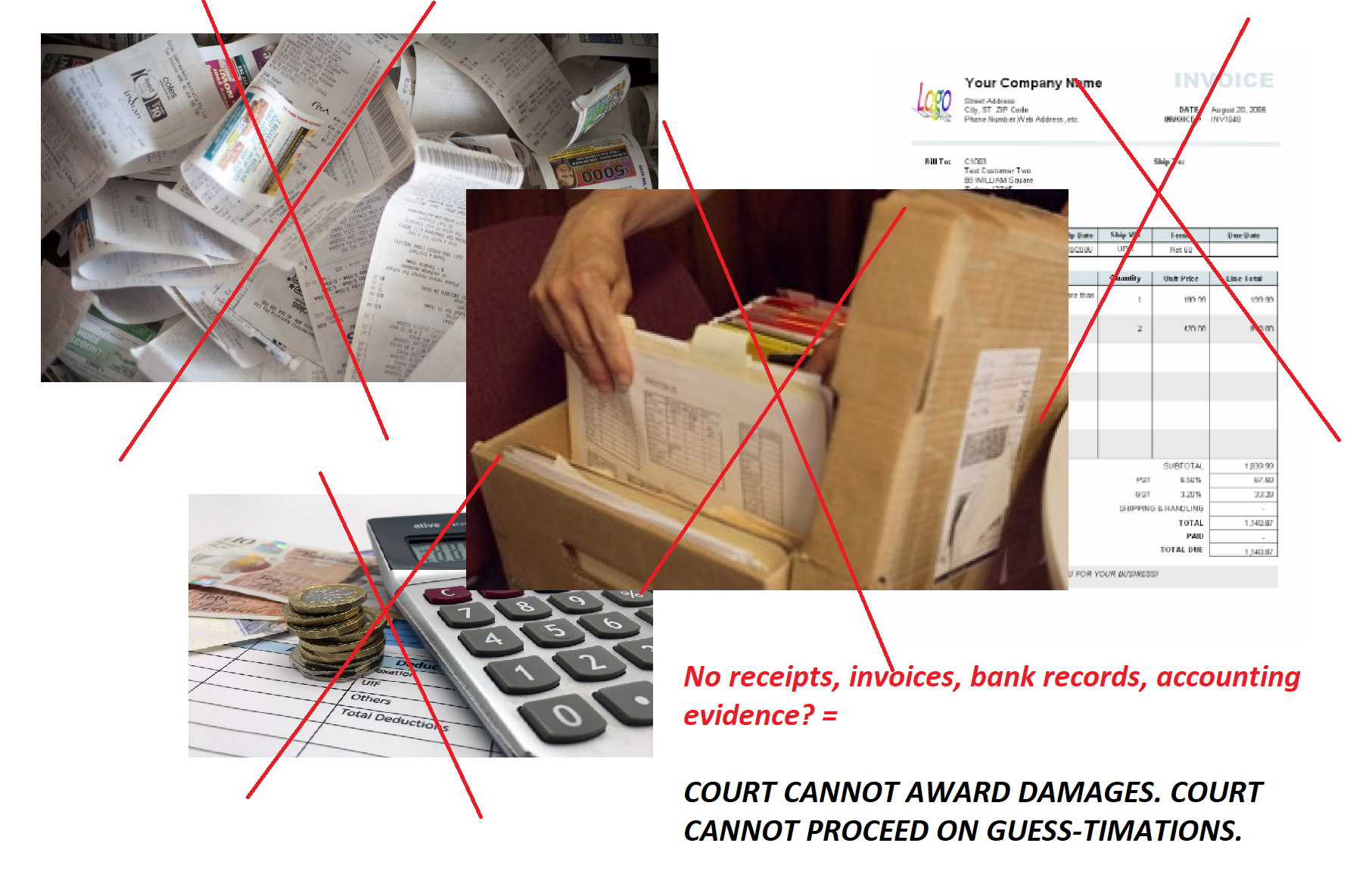

Rule of thumb:Can you claim a loss in Court with only estimations & no actual receipts/payslips/invoices/bank accounts showing the exact amount lost? No, if you cannot – in order to claim a loss successfully in Court you have to be able to refer to bank statements etc to show the basis for the amount lost, otherwise no award can be made. The Court cannot order someone to pay something on the basis of 'guess-timations'.

Background facts:

This case was in the subjects of the law of tax law generally, evidence and remedies. It invoked the principles of rebates, sufficient evidence and financial loss.

The basic facts of this case were very simple. NHS Lothian had a lab which provided services to the NHS which were exempt. The lab however also provided these similar lab services privately to the public, and charged for these services. Many years after doing this, NHS Lothian sought to reclaim a historic tax rebate on this as they only realised later that they qualified for an exemption which they did not know existed at the time, even though they should have. However, the legal issue was, NHS Lothian did not have any receipts and bank accounts records from this period as it happened so long ago – these had been destroyed.

Instead NHS Lothian sought to use other forms of record holding to estimate how much they would have paid, such as wear and tear in equipment, but not actual official financial documents. Although this was a tax rebates case, it was not actually tax law legal principles which were invoked in the case. HMRC argued that this was not sufficient evidence to infer the facts of the case, and this was certainly not sufficient financial evidence (receipts, bank records & an accountant’s report) to obtain a specific financial loss from them.

Moreover, if a litigant widely in litigation is wanting to claim money/debt owed for a specific loss, they have to be able to provide actual receipts or bank account details to demonstrate this, preferably compilated into a specific accounting report as well, or else they cannot be obtained, and a legal action should not be raised. Losses sustained cannot be estimated, instead they must actually be able to be shown with clear financial records. NHS Lothian were entitled to no tax rebate in these circumstances.

Judgment:

The Court upheld the arguments of HMRC. This case invoked 2 very simple but important principles of evidence and damages. A litigant must have ‘sufficient evidence’ to prove a significant fact, which is what claiming a very large amount of money is, namely direct evidence rather than circumstantial evidence, and NHS Lothian did not have this direct evidence, rather they only had circumstantial evidence as the direct evidence was lost, which is not sufficient evidence to prove a significant fact.

Ratio-decidendi:

‘89… If the taxpayer has either properly or foolishly destroyed the records it once held because of its own retention policies, that may prevent it from proving that it incurred the input tax which it now wishes to claim. The non-availability of evidence in such circumstances is a fact of life that often determines whether parties bring or refrain from bringing proceedings to enforce their rights in all areas of the law. 90. On this ground too, I would hold that HMRC’s appeal must succeed’, Lady Rose

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.