Haworth, R (on the application of) v Revenue and Customs [2021] UKSC 25 (2 July 2021)

Citation:Haworth, R (on the application of) v Revenue and Customs [2021] UKSC 25 (2 July 2021).

Subjects invoked: 11. 'Legal Methods'.81. 'Transactional taxes'.56. 'Investments'.

Rule of thumb:Is an in-point statutory provision enough legal justification for HMRC or the state generally to serve someone with a penalty notice? No, the Court affirmed that if someone has taken a ‘tax avoidance measure’ and declared this to HMRC, then HMRC is only allowed to send them a strict liability fine if there is an in-point statutory provisions combined with an in-point case – an in-point statutory provision only is not enough to serve someone with a penalty fine.

Background facts:

This case invoked the subjects of transactional taxes, professional services investment, and legal methods.

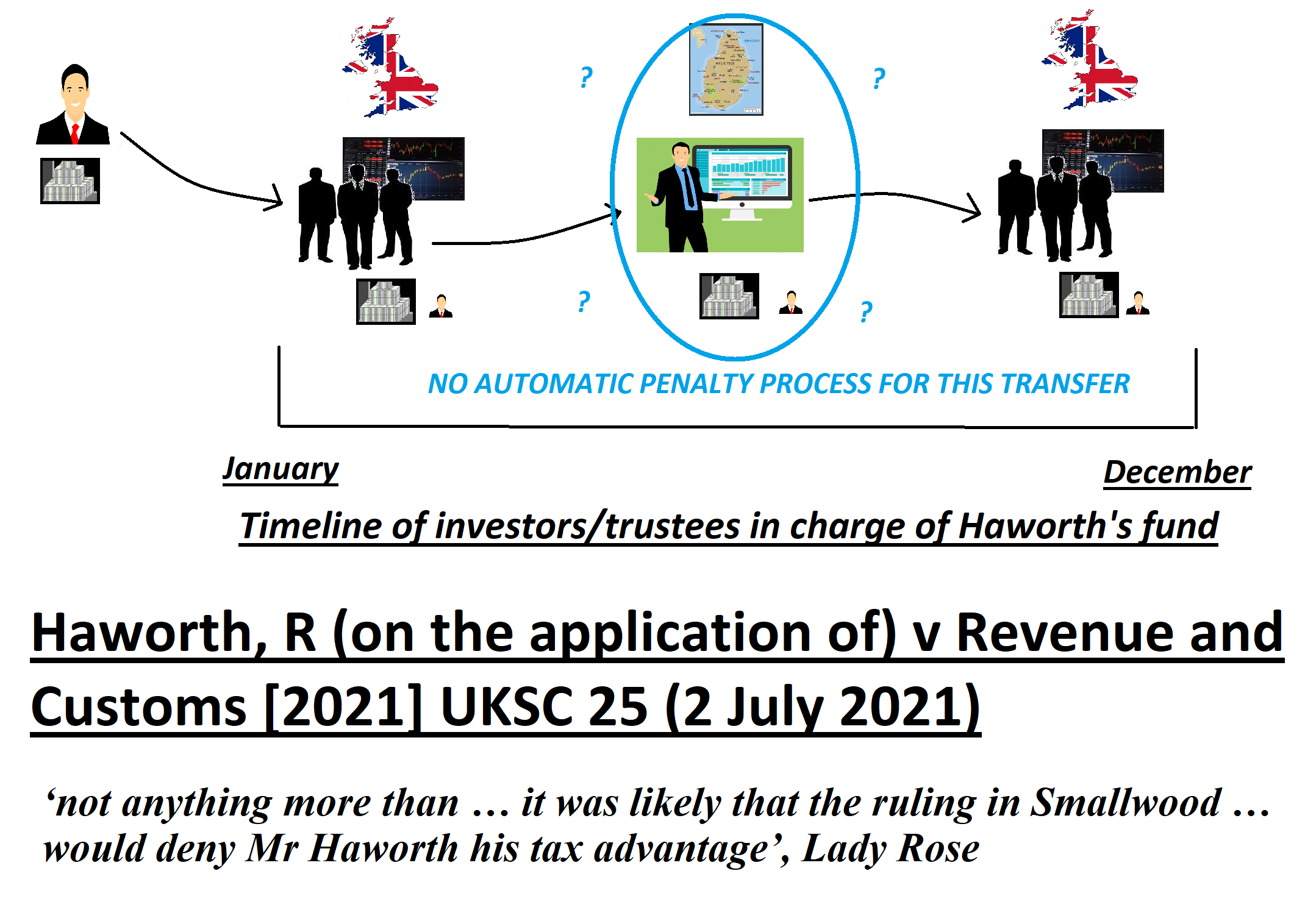

The material facts were that Haworth had a large fund of money and appointed UK trustees to oversee the investments from this fund. For what Haworth believed were valid strategic reasons related to expertise and windows of opportunity, Haworth wanted to change the investors to trustees in Mauritius for a period in the year, before UK trustees were re-appointed towards the end of the year. Haworth informed HMRC that during this period it was also coincidental that he would make a capital gains tax saving on the standard disposal of assets held by the trust, which he maintained was secondary to the expertise he sought from the Mauritius trustees.

HMRC informed Haworth that this approach was a clear breach of the law, substantiating their position with Smallwood v Revenue and Customs Comrs [2010] EWCA Civ 778, where appointing trustees in a foreign country purely to reduce capital gains tax was a breach of the law, and sent Haworth a ‘follower notice’ – stating that this was a blatant breach of the law and if he did not pay he would be subject to enormous financial penalties along the line. Haworth argued that this ‘follower notice’ was not appropriate and did not apply to his case as the circumstances could be distinguished from Smallwood – Haworth therefore sought a judicial review.

This case by and large came down to the legal methods principles of ‘inductive reasoning’ and ‘deductive reasoning’. ‘Deductive reasoning’ is when there is legal authority which is directly in point related to actions someone has taken, to make it a law that must unequivocally be followed by the lower Courts. Inductive reasoning is where there is authority which is only broadly in-point and can be used persuasively to make a legal argument, and could and perhaps should be accepted by the lower Court to support a legal position, but is not absolutely in-point.

HMRC argued that the Smallwood case was deductive reasoning in the Haworth case. HMRC argued that where a person sets up a fund in the UK with UK trustees, then appoints investor trustees in another country, which is a tax haven, for part of the year and makes a massive capital gains tax saving, before then switching back to the UK investors later in the year, then these technical reasons were not credible in these circumstances and this was ‘effective management’ from the UK. HMRC argued that Haworth and Smallwood were materially the same, and this was a blatant breach of the law by Haworth entitling them to issue a ‘follower notice’. Haworth argued that the Smallwood case was not deductive reasoning that applied to him. Haworth explained how his circumstances could be clearly distinguished from the Smallwood case - principally that his appointments of Mauritius investors were for legitimate expertise reasons, and CGT savings were purely incidental, and Smallwood as a legal authority against him was not in-point and deductive, and rather was only inductive and broadly supportive of a position against him. Haworth argued that given the severity of a follower notice, it was not appropriate to issue this to him when he still had arguments to make to explain his position.

Judgment:

The Court upheld the arguments of Haworth. They affirmed that even if the Smallwood ‘effective management’ case was strongly supportive of HMRC’s position, it was not absolutely in-point deductive reasoning. The Court further affirmed that even if the Smallwood case would make HMRC 80% strong favourites to win the case through very persuasive inductive reasoning, this authority was not absolutely in-point to take them up to the 99% certainty of winning the case level where a ‘follower notice’ is entitled to be issued. In short, the Court affirmed that ‘follower notices’ can only be issued by HMRC where there is strict deductive reasoning, not persuasive inductive reasoning.

Ratio-decidendi:

‘69. In the present case, Mr Stone fairly accepted that the evidence presented by HMRC does not support the conclusion that HMRC’s opinion was anything more than that it was likely that the ruling in Smallwood if applied would deny Mr Haworth his tax advantage…’, Lady Rose

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.