Macaura v Northern Assurance Co Ltd [1925] AC 619

Citation:Macaura v Northern Assurance Co Ltd [1925] AC 619

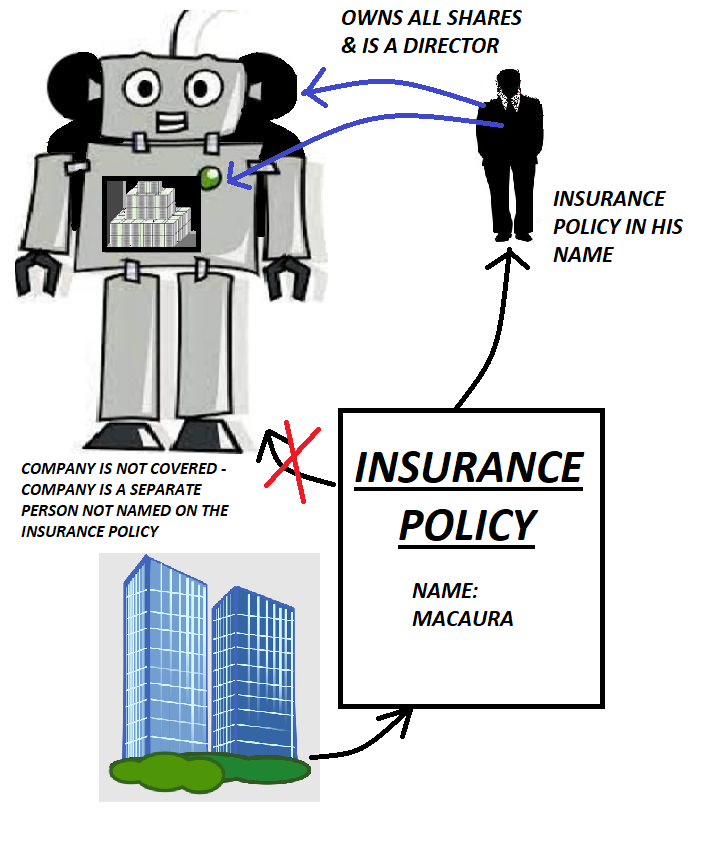

Rule of thumb:If a property insurance policy is bought and it is not in the name of the person who has ownership or occupancy of the property is it valid? No. Even if a person owns 100% of the shares in a company and is the only director, does separate personality still apply? Yes, it does. The Court in this case affirmed the fundamental principle of shareholders’ rights, and it also affirmed that even if someone is the 100% shareholder of a company this is still not an exception to the principle of separate personality. The Court affirmed that shareholders only have 3 fundamental rights in the company operations – (i) entitled to dividends (ii) entitled to vote at meetings, and then if the company is sold, (iii) an entitlement to their percentage share of the money generated by the company if it is sold or wound up and all its assets are converted into cash minus any debts. The Court affirmed that shareholders have no ownership in any of the company’s property, no property rights in relation say in how the company is run, and they are not liable for any debts.

Background facts:

The facts of this case were that Macaura 100% owned a business. When Macaura was organising the insurance for the business, he booked it in his own name and from his own bank account, rather than from the company bank account. The place where the business was being run ended up going on fire and it sought to rely on the insurance policy purchased by Macaura. The insurers refused to pay out on the basis that he did not own any of the property insured meaning that the insurance policy was not valid.

Parties argued:

Macaura argued that he basically was the company because he owned 100% of the shares in it meaning whether he bought it from his account or the company account did not matter.

Judgment:

The Court held that Macaura and the business were 2 different people – and the company did not have a valid insurance policy for its property. The company was not entitled to an insurance payout for the damage caused to its property by the fire.

Ratio-decidendi:

’the corporator even if he holds all the shares is not the corporation… neither he nor any creditor of the company has any property legal or equitable in the assets of the corporation.” ( Lord Wrenbury, at 633), ‘In the present case, though it might be regarded as a moral certainty that the appellant would suffer loss if the timber which constituted the sole asset of the company were destroyed by fire, this moral certainty becomes dissipated and lost if the asset be regarded as only one in an innumerable number of items in a company’s assets and the shareholding interest be spread over a large number of individual shareholders – Lord Buckmaster, ‘Now, no shareholder has any right to any item of property owned by the company, for he has no legal or equitable interest therein. He is entitled to a share in the profits while the company continues to carry on business and a share in the distribution of the surplus assets when the company is wound up. If he were at liberty to effect an insurance against loss by fire of any item of the company’s property, the extent of his insurable interest could only be measured by determining the extent to which his share in the ultimate distribution would be diminished by the loss of the asset – a calculation almost impossible to make. There is no means by which such an interest can be definitely measured and no standard which can be fixed of the loss against which the contract of insurance could be regarded as an indemnity...’ Lord Buckmaster, ‘My Lords, this appeal relates to an insurance on goods against loss by fire. It is clear that the appellant had no insurable interest in the timber described. It was not his. It belonged to the Irish Canadian Sawmills Ltd, of Skibbereen, co Cork. He had no lien or security over it and, though it lay on his land by his permission, he had no responsibility to its owner for its safety, nor was it there under any contract that enabled him to hold it for his debt. He owned almost all the shares in the company, and the company owed him a good deal of money, but, neither as creditor nor as shareholder, could he insure the company's assets. The debt was not exposed to fire nor were the shares, and the fact that he was virtually the company's only creditor, while the timber was its only asset, seems to me to make no difference. He stood in no "legal or equitable relation to" the timber at all. He had no "concern in" the subject insured. His relation was to the company, not to its goods, and after the fire he was directly prejudiced by the paucity of the company's assets, not by the fire’. . Lord Sumner

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.