Stanford International Bank Ltd v HSBC Bank PLC [2022] UKSC 34 (21 December 2022)

Citation:Stanford International Bank Ltd v HSBC Bank PLC [2022] UKSC 34 (21 December 2022).

Rule of thumb:If an investor is carrying out a Ponzi scam on investees’ funds, can the commercial bank the investor did this from who failed to notice red-flag behaviour be sued by the liquidator of the investment bank on behalf of investees? No, the liquidator does not have standing to represent the investees – the investees need to sue the bank on their own behalf if they feel the commercial bank missed behaviour which should have set off red flag warnings.

Rule of thumb:

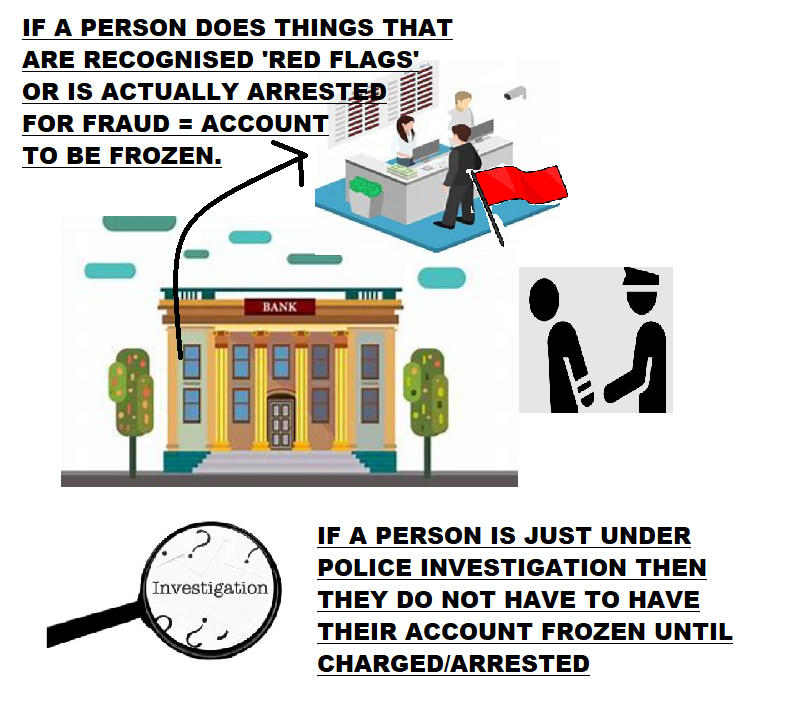

If a person is under criminal investigation, should their bank account be frozen? No, as a general rule it only has to be frozen once they are actually charged with a criminal offence, unless there are exceptionally clear warning signs of illicit activity which the bank should be picking up on.

Background facts:

The facts of this case were that Stanford Investments were an investment company who was running a Ponzi scam. Stanford Investment senior personnel were under police investigation, but were not formally arrested & charged with any offences. HSBC were the bank for Stanford. HSBC only froze Stanford’s bank account when Stanford senior personnel were formally arrested & charged by Police with the Ponzi fraud they were carrying out.

Parties argued:

Liquidators acting on behalf of Stanford’s trying to recoup as much money as possible for creditors/investors who invested money into the scam, and argued that HSBC should have had reasonable suspicion of Stanford’s Ponzi fraud before they froze the account, and that HSBC therefore owed some of the investors damages for not freezing the account sooner. HSBC argued that they were only a duty to freeze an organisation’s bank account once the organisation was actually charged.

Judgment:

The Court rejected the Stanford liquidators’ arguments. This case was not actually brought by any of the creditors, rather it was brought by Stanford. The Court affirmed that the bank had not actually caused the Stanford company itself any losses, so there was not actually any loss caused to the Stanford company, so the Stanford company themselves were not actually owed any money on a technicality – the individual who gave money to Stanford to be invested would be the ones who would actually have to raise the case rather than the insolvency practitioner.

It should be noted that if one of the investors themselves had raised the case it might have been different, but the liquidators who are actually representing Stanford were not entitled to raise this case. It should be further noted that Lord Sales dissented and believed that liquidators should be able to represent 3rd party creditors in this scenario, but the other 4 Judges disagreed.

Ratio-decidendi:

‘57. … the liquidators cannot have their cake and eat it on this point… 85… The short of the matter is that there are in my opinion no reasonable grounds for the claim that SIB suffered loss by making payments for which it received full value. For that reason its claim to recover (more than nominal) damages from HSBC must fail’, Lord Leggatt

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.