Revenue and Customs v SSE Generation Ltd [2023] UKSC 17 (17 May 2023)

Citation:Revenue and Customs v SSE Generation Ltd [2023] UKSC 17 (17 May 2023)

Rule of thumb:If you upgrade your business property/land, can you deduct this as a capital expense from profits to reduce corporation/income tax? Yes, as long as the expense spent on capital is not forbidden by a statutory provision then this is deductible provided it validly improved assets owned.

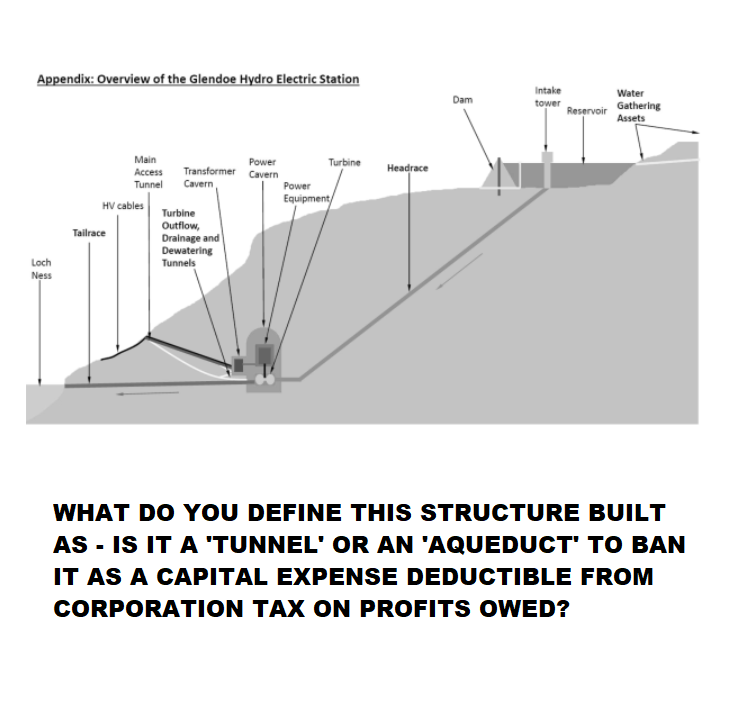

Background facts:The basic facts of this case were that SSE built a tunnel-type structure at a cost of £200 million. SSE then submitted a corporation tax return to HMRC affirming that this was deducted from their profits for the year to reduce the amount of income they owed by £40 million. HMRC stated that capital expenditure on this as a deductible expense was banned under the Capital Allowances Act 2001.

Parties argued:This case invoked the subjects of income tax & property. This debate essentially came down to looking up the dictionary definitions of ‘aqueduct’ & ‘tunnel’ which were expressly mentioned in the relevant tax Act and then looking at what was built to see if it actually was this. SSE argued that this was a valid expenditure on their assets which they were allowed to deduct from their profits as what they built did not fall within the dictionary definition of these words. HMRC argued that this was a tunnel or viaduct, both of which it was affirmed in statute was capital expenditure which was non-deductible.

Court held:After a long debate this case basically boiled down to a consideration of what this structure SSE built actually was & scrutinising the dictionary definitions of the words. The Court was satisfied that it was neither a tunnel or an aqueduct so it was not a banned deductible capital expense under the 2001. The Court therefore held that SSE were entitled to deduct the money they spent building this from their profits in calculating corporation tax.

Ratio-decidendi:

‘Other dictionaries give as their first or most common meaning of aqueduct a form of bridge-like structure for carrying water. For example, Oxford Dictionary of English (3rd edition): “a bridge or viaduct carrying a waterway over a valley or other gap”; Shorter Oxford English Dictionary (6th edition): “an artificial channel, esp. an elevated structure of masonry, for the conveyance of water”; Chambers Dictionary (13th edition): “an artificial channel or pipe for conveying water, most commonly understood to mean a bridge across a valley”; Cambridge Online English Dictionary: “a structure for carrying water across land, especially one like a high bridge with many arches that carries pipes or a canal across a valley”. As Rose LJ observed, a bridge-like structure for carrying water is what “comes immediately to mind”, an observation that reflects that common meaning. … For all the reasons set out above I reject HMRC’s suggested interpretation of both “tunnel” and “aqueduct”…’, Lord Hamblen

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.