Philipp v Barclays Bank UK PLC [2023] UKSC 25 (12 July 2023)

Citation:Philipp v Barclays Bank UK PLC [2023] UKSC 25 (12 July 2023)

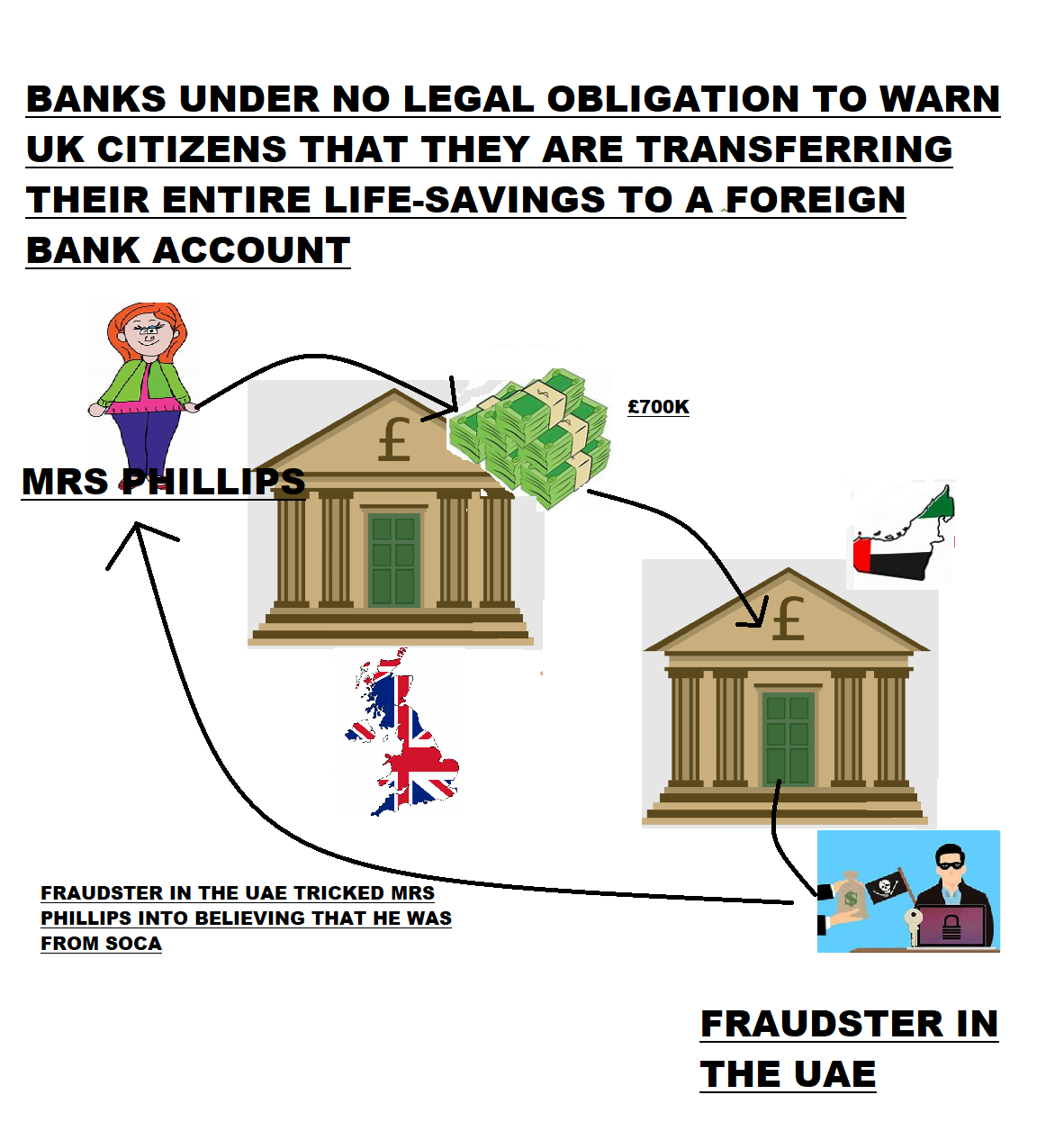

Rule of thumb:If you fall for a fraud and transfer money to another bank account in a foreign country, can you claim this money back from the bank because they did not warn you before you did it? No, if there was no warning on this other bank account for fraud then you cannot get this money back – it is lost, and it will be hard to prove your case as an exceptional circumstance where you can get the money back.

Background facts:The facts of this case were that Mrs Phillips fell for a fraudulent scam and transferred £700k from her Barclays bank account to a bank account in another country. Mrs Phillips sought Barclays to pay her back the money she transferred.

Parties argued:Mrs Phillips argued that with such a large transfer Barclays should have delayed the transfer and checked it out. She argued that they failed in their duty to do proper checks before sending the money. Barclays argued that there was no obligation on them to do this. Barclays affirmed that if there is an agency which the money has been transferred to, which it can be quite easy to set up an account with, then warnings have to be sent. However, they argued that when it is another bank account directly, which there is no flagged issue with, they were under no obligation to do this.

Court held:The Court upheld the arguments of Barclays. It affirmed that diligence of customer’s money did not require them to check the name & person of another person from the other account who money was being sent to, and check that there was a match, before allowing the transfer to go through. Mrs Phillips lost her £700k.

Ratio-decidendi:

‘The last of these circumstances would include a situation where the Bank reasonably believes that a payment instruction given by the customer is the result of APP fraud. In accordance with this express term of the contract, the Bank therefore had a right in that event to decline to carry out the instruction. Having such a right, however, is obviously not the same as being under a duty. Pursuant to this term, the Bank was entitled to decline to carry out the instruction given by Mrs Philipp on 19 March 2018 to make a third transfer of funds to the UAE, having been told by the police on 16 March 2018 that her current account had been compromised by fraudsters in the UAE (see paras 13-14 above). Were it not for that contractual term, Mrs Philipp could potentially have sued the Bank if the result of its refusal to carry out her instruction had been to cause her loss (instead of being, as was actually the case, to save her from losing even more money). It remains to consider a fallback argument made by the claimant that the Bank was in breach of duty after the fraud had been discovered in not taking adequate steps to recover the money which had been transferred to the UAE. Having decided the main issue in Mrs Philipp’s favour, the Court of Appeal did not think it necessary to address this point separately. But on the view I take that the Bank cannot be faulted for carrying out Mrs Philipp’s instructions to make the transfers, it becomes relevant to do so’, Lord Leggatt at 114-115.

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.