Sharp Corp Ltd v Viterra BV [2024] UKSC 14 (08 May 2024)

Citation: Sharp Corp Ltd v Viterra BV [2024] UKSC 14 (08 May 2024)

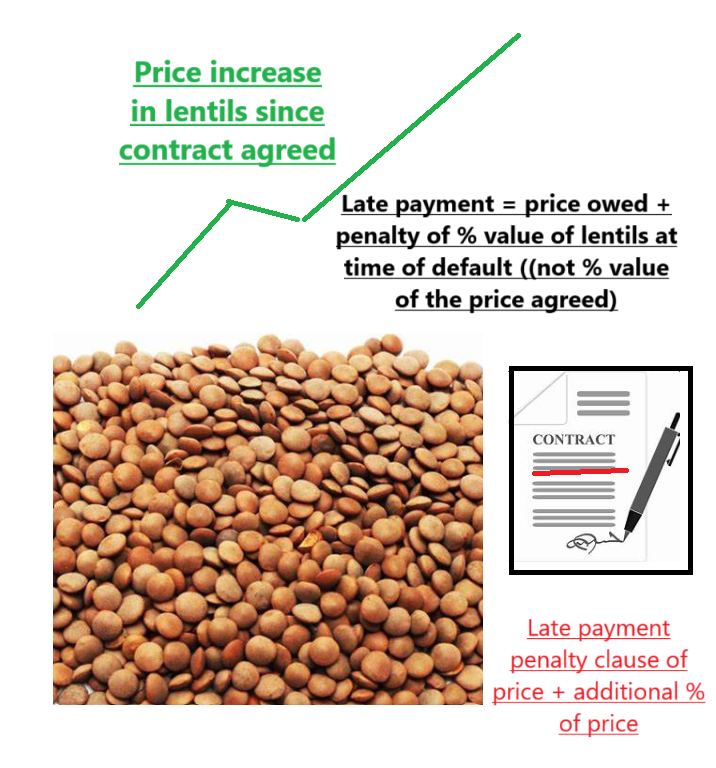

Rule of thumb: If you default on a contract & there is a penalty clause related to the value of the goods, is this the value of the goods on the date of default or the original date of the contract being agreed? The value which the % penalty is to be applied on is the default date – this means that if the value of the goods has gone up or down at the point of default then the penalty clause may be more or less than first anticipated when the contract was first agreed.

Background facts: This case invoked the subjects of movable property & contract law.

The facts were that Viterra, based in Canada, sold peas & lentils to Sharp Corp, based in Italy. Viterra shipped these out to India, but Sharp had still not paid the money owed for these. Viterra therefore held the peas & lentils in cold storage. There was a term of the contract which stated that if the price was not paid a penalty on a % value of the goods had to be paid in addition to the original price agreed. The cost of peas & lentils had jumped up hugely in this time, so the penalty clause applied on the original date of the contract being agreed was much higher.

Court held: The Court held that it was the value of the goods at the date of default which the % penalty clause had to be taken from – it was the higher rate of penalty Sharp owed – this case had to be remitted so that the exact price on the default date could be ascertained by expert evidence.

Ratio-decidendi:

'This answer assumes that there was an available market for sale of the goods in bulk ex warehouse Mundra on or about the default date. There are suggestions in the Awards that the evidence did not show that there was a market for a sale of the goods in bulk but only of parcels over time which would mean by reference to market prices which would no longer reflect that prevailing on the default date. It may nevertheless be possible to extrapolate a bulk price from the market evidence of prices on the default date. Even if it is not and it is concluded that there was no available market, the estimated value of the goods should be assessed on the basis of the goods as and where they were on the date of default - ie customs cleared in a warehouse in Mundra. Those were the goods which were left in the Sellers' hands and it is their realisable value that should be used to establish the default price. That reflects the reality of the position in which the Sellers found themselves as a result of the Buyers' non-acceptance’.

Lord Hamblen

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.