Test Claimants in the Franked Investment Income Group Litigation v Revenue and Customs [2021] UKSC 31 (23 July 2021)

Citation:Test Claimants in the Franked Investment Income Group Litigation v Revenue and Customs [2021] UKSC 31 (23 July 2021).

Subjects invoked: 13. 'Remedies'.80. 'Income tax'.

How much damages are companies affected by the 'franked investment income' tax breach owed? The answer frankly is that it is complicated... This case essentially affirmed 6 points of law related to how much damages foreign parent companies with subsidiaries in the UK, or UK parent companies with subsidiaries abroad, were entitled to because of the unfair rollover system HMRC implemented which financially benefited UK holding companies exclusively with subsidiaries in the UK. This case invoked very large damages, and the test claimants, BAT and FCE, were making arguments to maximise these damages, and HMRC were making arguments to minimise the damages, and both had some points upheld by the Court.

Background facts:

This case invoked the subjects of income/corporation tax and remedies.

2 past cases related to this one, and they have to be known in order to understand the case at hand. The first case, Pirelli Cable Holding NV v Inland Revenue Comrs [2006] UKHL 4, affirmed that HMRC owed some UK holding companies with foreign subsidiaries, and UK subsidiaries of foreign holding companies, damages. HMRC owed these companies damages because HMRC did not allow these companies to implement full roll-over relief on their company group losses for corporation tax, but they did allow full rollover relief for UK holding companies with only UK subsidiaries. This system was deemed to be a breach of the law in this case. Secondly, in Test Claimants in the Franked Investment Income In Group Litigation & Ors v Revenue and Customs [2020] UKSC 47, it was further held that the time-bar limit of 6 years backdated from the date of this case against HMRC being raised, applied to the losses sustained because of the roll-over system, rather than the 30 odd years the system had been in place and been enforced by HMRC. This second case of course greatly reduced the damages that HMRC would potentially have to pay these UK holding companies with foreign subsidiaries or UK subsidiaries of foreign holding companies for doing this.

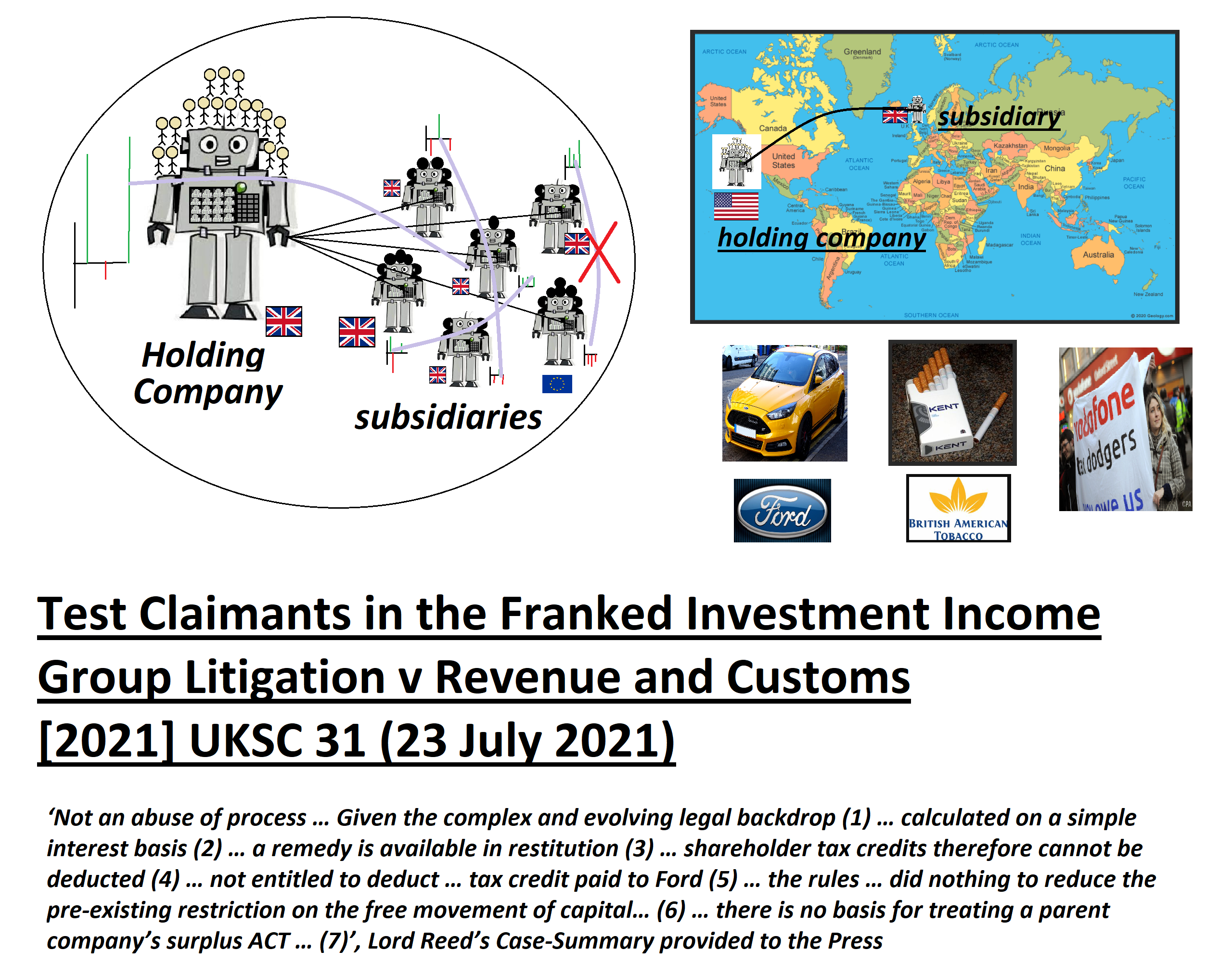

The test claimants were British American Tobacco and Ford. British American Tobacco essentially set up factories to manufacture cigarettes and sell them. Ford basically set up factories to make cars and garages to sell them, as well as set up financing for the purchase of these cars. In their company groups both of them had companies registered in different countries, rather than just registering all of their companies in the UK, and this meant that due to the roll-over relief system HMRC operated for exclusively British holding companies and subsidiaries, Ford and British Tobacco paid extra corporation tax in the UK.

Before explaining the facts & legal issues of this case the nature of a ‘holding company & subsidiary’ relationship is provided (please note a ‘holding company’ and a ‘parent company’ mean the same thing). A ‘holding company subsidiary’ relationship exists where one company holds a majority stake in the shares of another company i.e. the ‘holding’ company holds shares of at least 51% in the ‘subsidiary’ company, meaning that the holding company has the power to appoint and dismiss the directors in this subsidiary company at the ‘Annual General Meeting’ (AGM). ‘Holding companies’ with many subsidiaries are a ‘company group’.

In addition, it is important to understand one of the ways the ‘holding company and subsidiary company’ relationship works. Larger companies with excess capital often invest in promising ‘projects’ proposed to them - these large companies provide the finance for these smaller companies’ projects and take at least 51% stake of their shares, thereby becoming the ‘holding company’ of this now ‘subsidiary’. The holding company then appoints the directors in this subsidiary, the subsidiary gets on with the project, and if the subsidiary company makes profits it typically pays corporation tax before giving the holding company dividends. It is also important to understand the concept of rollover relief/tax credits. This means that if a company makes a £250k loss in 2005, and then makes £1 million in profits in 2006, they rollover their 250k loss onto the next year’s £1 million profits, and only pay the corporation tax rate of 20% on £750k of the profits (1 million profits – 250k past year losses) rather than on the full 1 million pounds of profits. In other words, 20% of 750k profits rather than 20% of 1 million profits is paid by the company, so their corporation tax bill is £150k rather than £200k. It is also important to understand that under the previous UK tax/accounting system company groups, where a holding company was based in the UK and so were all its subsidiaries, the holding company and the subsidiaries in the group could roll their losses over onto each other. This was shown to massively reduce the corporation tax large holding companies had to pay. Some massive holding companies with lots of subsidiaries paid next to no corporation tax for many years in the UK with this system in place. The UK corporation tax rate on paper was 20%, however, for large holding companies it was in reality much, much lower than this.

The key fact of this case was that the HMRC only allowed company groups where the holding company was based in the UK and so were all its subsidiaries to fully roll-over losses like this. UK companies with foreign parent companies were not allowed to implement this roll-over of losses system, and UK holding companies with foreign subsidiaries could not do this either. This failure to allow all the company groups to roll-over losses, and only allow UK companies to do this, was what was deemed to be a breach of the law by HMRC in cases in the past.

This rollover system for UK holding companies and their UK subsidiaries was because of UK accounting rules called the ‘Advanced Corporation tax’ (ACT) system in the Income and Corporation Tax Act 1988. Section 18, Part VI, Schedule D, Case V (called ‘DV’ for short), of the 1988 Act was the key section that put this maligned rollover system in place. This was essentially the rule that allowed this loss rollover/ tax credit system to take place fully in UK company groups. This UK accounting ‘DV’ rule, giving full rollover relief only to UK holding companies and UK subsidiaries, meant that UK company groups could fully carry forward losses from previous years in any of their UK companies, and use them to reduce the amount of corporation tax to be paid on the profits of any company in the group, before dividends were paid out, but this could not be done if the parent company was from the EU or the USA, or fully if a UK holding company had foreign subsidiaries.

This meant that UK subsidiaries with EU or US holding companies, or UK holding companies with foreign subsidiaries, paid a lot of extra tax to HMRC because of this. HMRC’s implementation of this system was deemed to have been a breach of the law. The UK Supreme Court in 2020 had previously stated that the damages caused by this scheme could only apply for the 6 year time-bar limit, rather than the full 30+ years that the UK had been operating this system however. Other aspects of how much HMRC had to pay in damages were decided in this case.

The legal issues

subsidiaries, with HMRC seeking to minimise damages, and Ford seeking to maximise damages. In this case there were essentially 7 questions about the amount of damages HMRC owed for implementing this rollover relief system: 1. Can the question of compound interest to be paid on any damages sum be challenged by HMRC, or is it too late as HMRC should have been challenged in previous cases? 2. What rate of interest is to be paid on any sum of damages? 3. What remedy does EU law expect in these circumstances? 4. Has HMRC actually caused any losses to them which can be reclaimed? Can HMRC smuggle out of having to pay damages on a technicality under the law of remedies? 5. Does it matter if the foreign parent company/holding company of the subsidiary was able to write off some of the losses of their UK subsidiary in their own country? 6. Is there any other way that HMRC can argue that what they did was legal? Challenge the case on liability based on new rules they have found? 7. Can losses from any foreign companies related to the UK subsidiaries, such as their foreign parent company, be rolled over for these years to reduce the tax-bill the UK would have had to pay?

Judgment:

The Court held the following 7 points: 1. Yes, HMRC can challenge this point of law. In complex cases like the one at legal arguments which were not thought up previously can be raised at a later; 2. The simple rate of interest and not the higher Judicial rate was to be paid on the sums owed to these UK subsidiaries with foreign parent companies; 3. EU law requires HMRC to pay the affected parties damages/restitution for the extra tax they paid; 4. HMRC were deemed to be enriched as a result of this and have to pay damages. The English law arguments about the UK subsidiaries with UK parent companies being under-charged, and UK with EU or other parent companies being charged the correct amount, meaning there was not actually any damage caused, were not accepted. HMRC owe the damages for this; 5. What these subsidiaries’ foreign parent companies have done in their own tax system, in terms of writing off some of the subsidiaries’ losses against their own profits, is of no relevance in calculating damages; 6. The case on the liability of HMRC is decided and final. HMRC cannot escape having to pay damages on what they owe on the basis of these rules; 7. It is only UK subsidiaries who are able to use rollover relief. Losses made by their foreign parent company or other foreign companies in their group cannot be rolled over to reduce the UK subsidiaries’ tax liability.

Ratio-decidendi:

‘JUDGMENT The Supreme Court unanimously allows the Revenue’s appeal on issues 1 and 2 above but dismisses their appeal on issue 4. The Supreme Court unanimously allows the Claimants’ appeal on issues 3, 5 and 6 above but dismisses their appeal on issue 7. Lord Reed and Lord Hodge give the judgment with whom Lord Briggs, Lord Sales and Lord Hamblen agree’. 1…. Further, the Revenue’s challenge does not amount to an abuse of process. Given the complex and evolving legal backdrop to the FII Group Litigation and related proceedings, it is unsurprising that questions of central importance have only recently or are yet to be decided [77-78]. 2. The Revenue’s case is that interest for the prematurity period should be calculated on a simple interest basis under section 85 of the Finance Act 2019 (the 2019 Act)… 3. … In respect of MCT already incurred as a result of the inability to carry forward DTR, a remedy is available in restitution to recover the MCT plus interest subject to the law of limitation [155-156, 158]. 4. … The shareholder tax credits cannot therefore be deducted from the unlawful ACT in calculating the compensation due to the Claimants. 5. … The Revenue are not therefore entitled in calculating compensation due to FCE to deduct from the unlawful ACT, the tax credit paid to Ford US [198]. 6. the introduction of the Eligible Unrelieved Foreign Tax Rules (EUFT rules) in 2001. … The rules introduced materially different procedures for the calculation of tax credits and did nothing to reduce the pre-existing restriction on the free movement of capital. As a result, the benefit of the standstill provision is lost… 7. … The ACT provisions deem the subsidiary to be the entity which has paid the surrendered ACT. They do not treat the parent company’s ACT liability as if it belonged to the corporate group as a whole [230]. There is therefore no basis for treating a parent company’s surplus ACT which was actually surrendered to a particular subsidiary other than as partly lawful and partly unlawful on a pro rata basis [232]’

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.