Crown Prosecution Service v Aquila Advisory Ltd [2021] UKSC 49 (03 November 2021)

Citation:Crown Prosecution Service v Aquila Advisory Ltd [2021] UKSC 49 (03 November 2021).

Subjects invoked: 7. 'Company'.43. 'Insolvency'.

Rule of thumb:If a former company director carries out fraud, is the company allowed to join the list of creditors in the former director's bankruptcy process?

Background facts:

This case invoked the subjects of insolvency law and company law.

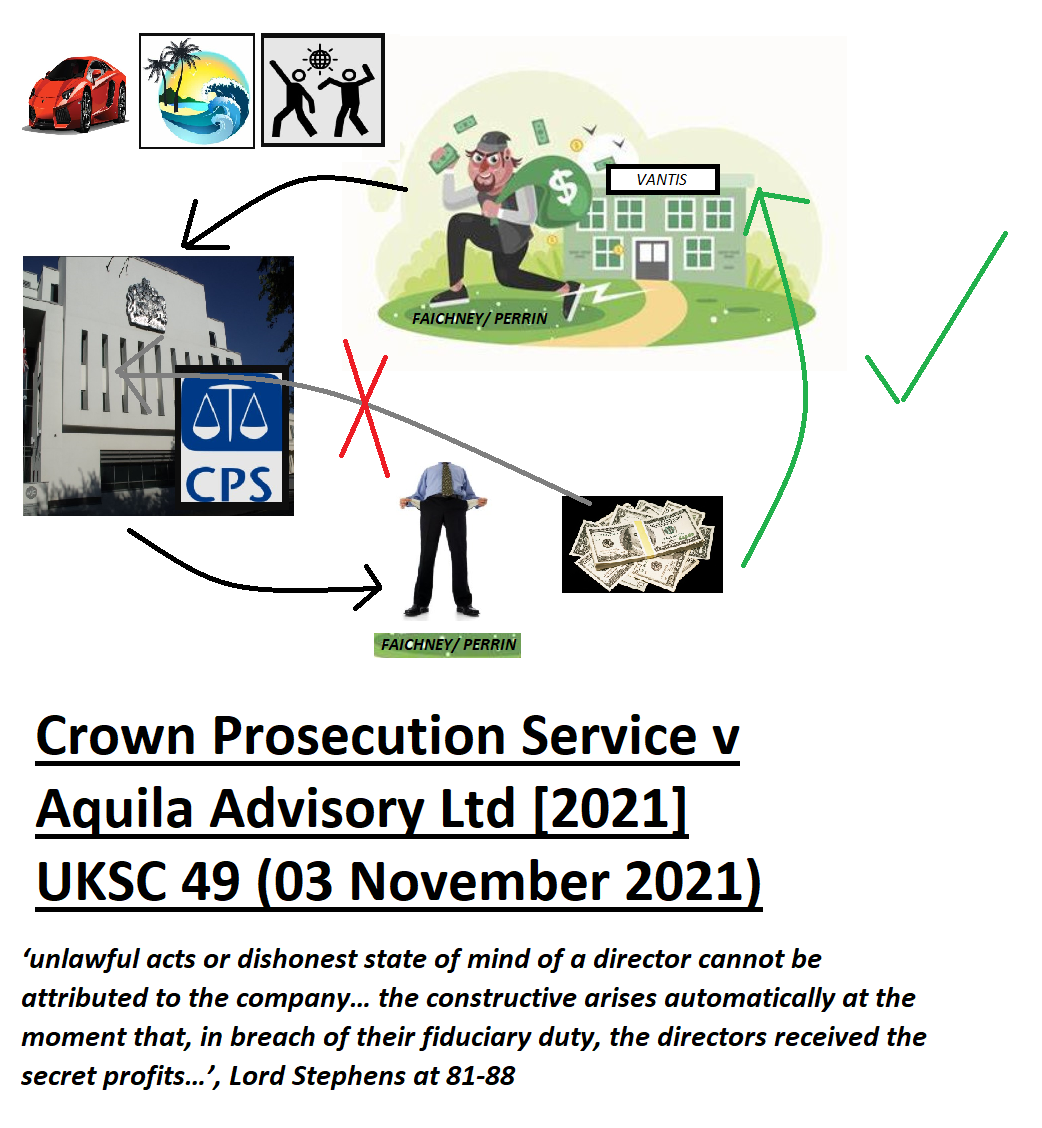

The facts of this case were that 2 ex-HMRC tax investigators, Mr Faichney and Mr Perrin, left HMRC to work for a tax advisory services company called ‘Vantis Tax Ltd’. In their new role for Vantis, these directors advised clients about what they said was a legal tax avoidance scheme. They informed clients they had worked for HMRC and knew that it was a legal arrangement. They took a commission on the massive tax savings they made for their clients, totalling around £4.5m in income. It later transpired that this tax advisory scheme they advise was fraudulent.

When this transpired the contracts of these directors were terminated at Vantis. Both were also successfully prosecuted. ‘Proceeds of crime’ officials within the Crown Prosecution Service calculated that these 2 individuals had taken £4.5 million in income from advising these fraudulent schemes, which they were not entitled to. The Prosecution Service claimed this money back from these individuals but they could not pay it, claiming they had spent virtually all of it, with only £810 and £650k left (£1.46m). Both were then declared bankrupt and an ‘accountant in bankruptcy’ was appointed to take over all of their bank accounts and assets.

After Faichney and Perrin were made bankrupt and the accountant in bankruptcy took over all of their remaining money and assets, the company in which these 2 individuals worked, now acquired by a company called ‘Aquila’ (who raised this case), put in a claim to the accountant in bankruptcy. They stated that they were entitled to the £1.46m these 2 former directors had left, as this was their money which those directors were only acting as trustees over. The Crown Prosecution Service thought that this was ridiculous that the company where these individuals carried out their fraudulent behaviour should be allowed to gain profits from these acts of tax fraud, essentially meaning that Aquila would gain and obtain money through a fraudulent enterprise. They therefore tried to obtain a declaration that they were entitled to obtain the £1.46m instead. Aquila challenged this and the matter proceeded to Court.

The Crown Prosecution Service argued that the contract law principle of illegality prevented Aquila from being able to acquire any of the money made by these 2 individuals. They argued that this principle meant that no person is able to gain any money/profits from their own illegal acts. They argued that this illegality principle applied to Aquila, as both they and the individuals had worked together to get this illegal money, and that they should not be allowed to take a share of it. They further argued that the Proceeds of Crime Act gave them priority over Aquila in this matter. They sought a declaration from the Court upholding this.

Aquila argued that illegality did not apply to this. They argued that it is clearly affirmed in law that directors acting criminally is deemed to be their decision as an individual, and not attributable to the company, and the circumstances of the case did not give rise to a position where there would be an exception to this. They also argued that directors are technically acting as trustees of the company’s assets/property and money, and they had wrongfully and criminally taken it from them. They also argued that under the law of trusts and insolvency, this gave them priority over the Criminal Prosecution Service. They sought a declaration from the Court stating that they were entitled to the £1.4m.

Judgment:

The Court upheld the arguments of Aquila. They affirmed that when directors act in a criminal manner illegality does not apply to the company, rather this is deemed to be solely the act of the individuals involved. It will only be on rare occasions when fraud is so widespread across the company that the company itself will be deemed to be fraudulent. The Court further affirmed that these directors were acting as trustees for their money, and in an insolvency procedure trustees are given priority with property returned to the original owner. Aquila were deemed to be the person entitled to the £1.44m. The Court affirmed that the reasoning of its previous case-law on this matter was sound and should not be overturned as CPS were arguing. They also stated that statutory provisions that the CPS were not in point and did not overturn the insolvency in the matter.

Ratio-decidendi:

Lord Stephens Ratio Decidendi at 81-88 ‘81. … Bilta is authority for the proposition that the unlawful acts or dishonest state of mind of a director cannot be attributed to the company so as to afford the director an illegality defence to the company’s claim against him for breach of fiduciary duty. The principles of illegality in Patel simply do not arise… 86. … The CPS has not availed itself of remedies under Parts 2 and 5 POCA. It is not permissible to use public policy considerations said to derive from Part 7 to alter the existing property rights under a constructive trust… 88… In other words, in this context, the constructive trust (and the principal’s beneficial ownership of the property) arises automatically at the moment that, in breach of their fiduciary duty, the directors received the secret profits. There was never a moment at which the former directors as fiduciaries owned the profits in equity. The declaration granted by Mann J not only has the effect of recognising this state of affairs but also accords with the terms of the settlement agreements entered into by the CPS…’

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.