Revenue and Customs v NCL Investments Ltd & Anor [2022] UKSC 9 (23 March 2022)

Citation:Revenue and Customs v NCL Investments Ltd & Anor [2022] UKSC 9 (23 March 2022).

Subjects invoked: '80. Income Taxes'

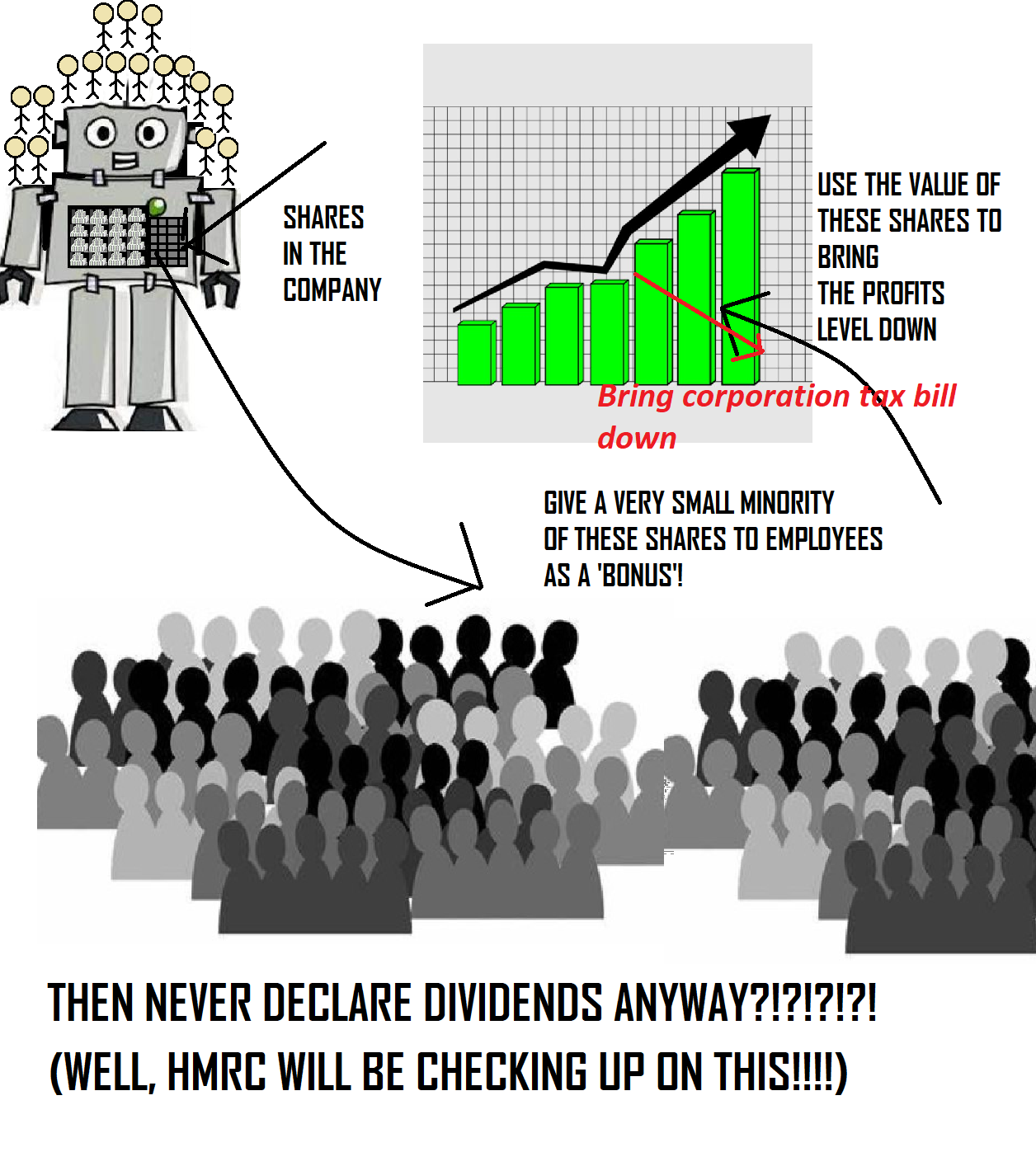

Rule of thumb:If a company has big profits one year, can they do a share issue to employees (which does not actually lead to the transfer of any money as such to employees), and then deduct the value of these shares from profits & corporation tax bill? Yes! This is a valid means of a company reducing their corporation tax bill. NCL in this case had large profits, gave a share bonus to employees, which cost them no money, got an accountant to value what the shares they issued to employees were worth on paper, and then deducted this value from their profits to pay less corporation tax.

Background facts:

This case invoked the subject of income taxes – in particular corporation tax, as well as to some degree employment law & company law. In particular it invoked the principle of whether a company giving a share issue to its employees was a deductible expense from profits to reduce a company’s potential corporation tax bill.

The facts of this case were that NCL Investment made a lot of profits one year. They offered their employees a share option i.e. they would go to companies house and transfer the employees shares which the company currently owned, which would mean the employees got money if the company ever gave out dividends, but it did not entitle the employees to any money there and then. Some employees sought to take this share option up and were transferred company shares. NCL got an accountant to calculate what the company shares were worth and what the value of the shares they had given employees was. They then deducted this amount from their profits and sought to reduce their corporation tax bill.

HMRC argued that this practice was banned under sections 1290-1297 of the Corporation Tax Act 2009. HMRC argued that no money was actually transferred to the employees, and employees were not liable to pay income tax or national insurance on the value of these shares, essentially meaning that this money was not taxed. They also further argued that the NCL may never even give out dividends, meaning that this was just a dodge of tax, and a practice which was forbidden under section 1290-1297. NCL argued that this practice was allowed by these 1290-1297 of the Corporation Tax Act. They argued that these sections were specifically introduced to allow this practice, as it was done on the rationale that it incentivised employees better, and that these sections had to be interpreted with the purpose behind them understood.

Judgment:

The Court after studying the statutory provisions carefully in light of the purpose behind them decided that this practice of share-offering to employees was not banned in general and NCL were allowed to implement this. The Court affirmed that companies are allowed to reduce their corporation tax doing this if they so desire. NCL only had to pay the reduced corporation tax bill. However, the Court did state that if indeed many years passed and the company indeed never gave out dividends, then HMRC may still be able to charge the company for this tax in the future.

Ratio-decidendi:

‘…there may be cases falling within section 1291 where in the event the deduction never becomes allowable, as was envisaged by Lord Hoffmann in Dextra. But we also do not accept Mr Ghosh’s underlying policy argument that we should strive to apply section 1290 to disallow the deduction of the Debits because the Options are not taxable qualifying benefits in the hands of the employees. We do not accept his description of sections 1290-1297 as a statutory code aimed at ensuring that relief for employee benefit contributions is only available if and when matched by a corresponding charge to income tax and national insurance contributions. On the contrary, Parliament has adopted a policy of encouraging employee share option schemes by providing that the options do not create a charge to income tax. In so giving with one hand, it does not appear to have taken away with the other hand by defining ‘employee benefit contribution’ in a way which has the effect of disincentivising employers by disallowing the deduction of the Debit as an expense in calculating corporation tax profits. The source and evolution of this provision set out in HMRC’s written case does not support the contention that it was intended to apply to the present circumstances’, Lord Hamblen at 73

Warning: This is not professional legal advice. This is not professional legal education advice. Please obtain professional guidance before embarking on any legal course of action. This is just an interpretation of a Judgment by persons of legal insight & varying levels of legal specialism, experience & expertise. Please read the Judgment yourself and form your own interpretation of it with professional assistance.